GIFT City is often spoken of as a single opportunity zone. In practice, it is three legally and regulatorily distinct jurisdictions operating inside one geographical boundary. Most business failures, licensing rejections, and tax disappointments in GIFT City arise from one basic mistake, treating GIFT City as one uniform regime.

From a business perspective, GIFT City only starts making sense when you stop asking “What benefits does GIFT City offer?” and start asking “Which GIFT jurisdiction does my business legally belong to?” That single classification determines your regulator, your compliance burden, and whether you receive any tax or GST benefit at all.

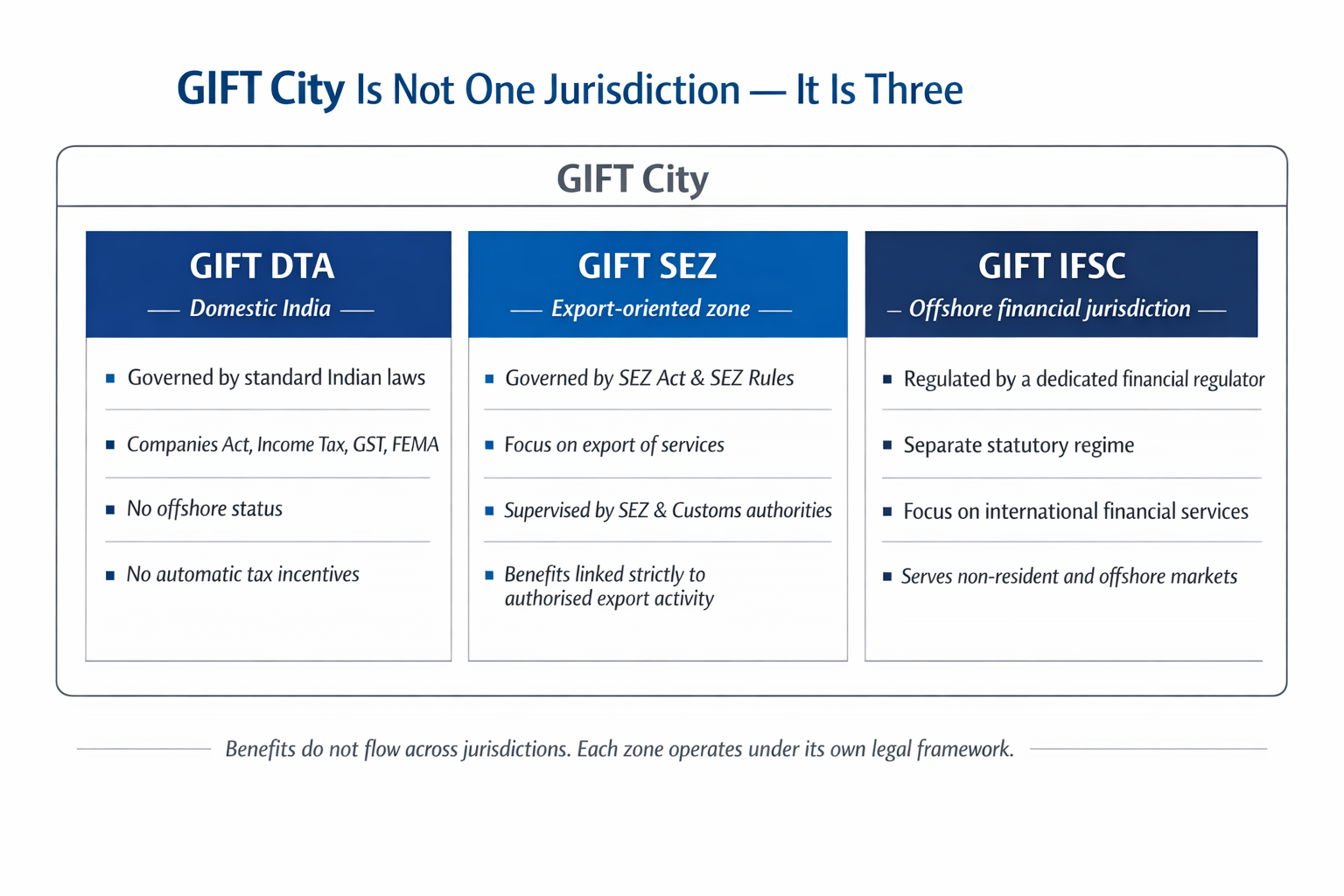

GIFT City Is Not One Jurisdiction — It Is Three

Legally and regulatorily, GIFT City does not function as a single economic or compliance zone. It operates through three distinct jurisdictions—GIFT DTA, GIFT SEZ, and GIFT IFSC—each created under a separate legal framework and designed to serve a different policy objective. These are not interchangeable labels or marketing constructs; they are formal legal classifications that determine how an entity is regulated, taxed, and supervised.

GIFT DTA represents the domestic side of GIFT City. From a legal standpoint, it is treated like any other part of India and is governed by standard Indian laws relating to companies, taxation, GST, and foreign exchange. There is no offshore treatment, no sector-specific regulator, and no automatic tax incentive merely because the business is located within GIFT City limits.

GIFT SEZ, by contrast, is an export-oriented enclave governed by the SEZ Act and the SEZ Rules. Its regulatory focus is not on the nature of the industry but on the export of services and foreign exchange earnings. Businesses operating in GIFT SEZ are supervised by SEZ authorities and customs, and they receive benefits only to the extent their operations qualify as authorised, export-linked activities under the SEZ framework.

GIFT IFSC occupies a fundamentally different legal position. Although it is physically located within the SEZ, it is regulated as a separate offshore financial jurisdiction under a dedicated statutory regime. Entities operating in IFSC are governed by financial-sector regulations and licensing requirements that do not apply elsewhere in India. The focus here is not exports in the traditional sense, but the provision of international financial services to non-residents and offshore markets.

Understanding this separation is critical because benefits do not flow horizontally across these jurisdictions. A tax or GST benefit available to an IFSC-regulated financial entity does not automatically extend to a SEZ unit or a DTA entity operating next door. Similarly, SEZ benefits are strictly linked to export activity and do not apply to domestic operations or non-SEZ units within GIFT City. Each benefit is tied to the legal status of the entity and the jurisdiction it operates in, not merely to its physical presence in GIFT City.

This structural separation is the foundation of the GIFT City framework. Ignoring it leads to incorrect expectations, rejected applications, and post-setup tax exposure. Understanding it upfront allows businesses to choose the correct zone, structure their operations lawfully, and access incentives that genuinely apply to their business model.

Regulatory Control: Who Regulates What, and Why It Matters

Regulatory control within GIFT City follows the same principle as its legal structure: regulation attaches to jurisdiction, not geography. Merely being located in GIFT City does not subject a business to any special regulator unless its activity legally falls within a defined zone. This distinction becomes critical when businesses assume regulatory flexibility or tax advantages without understanding who actually supervises their operations.

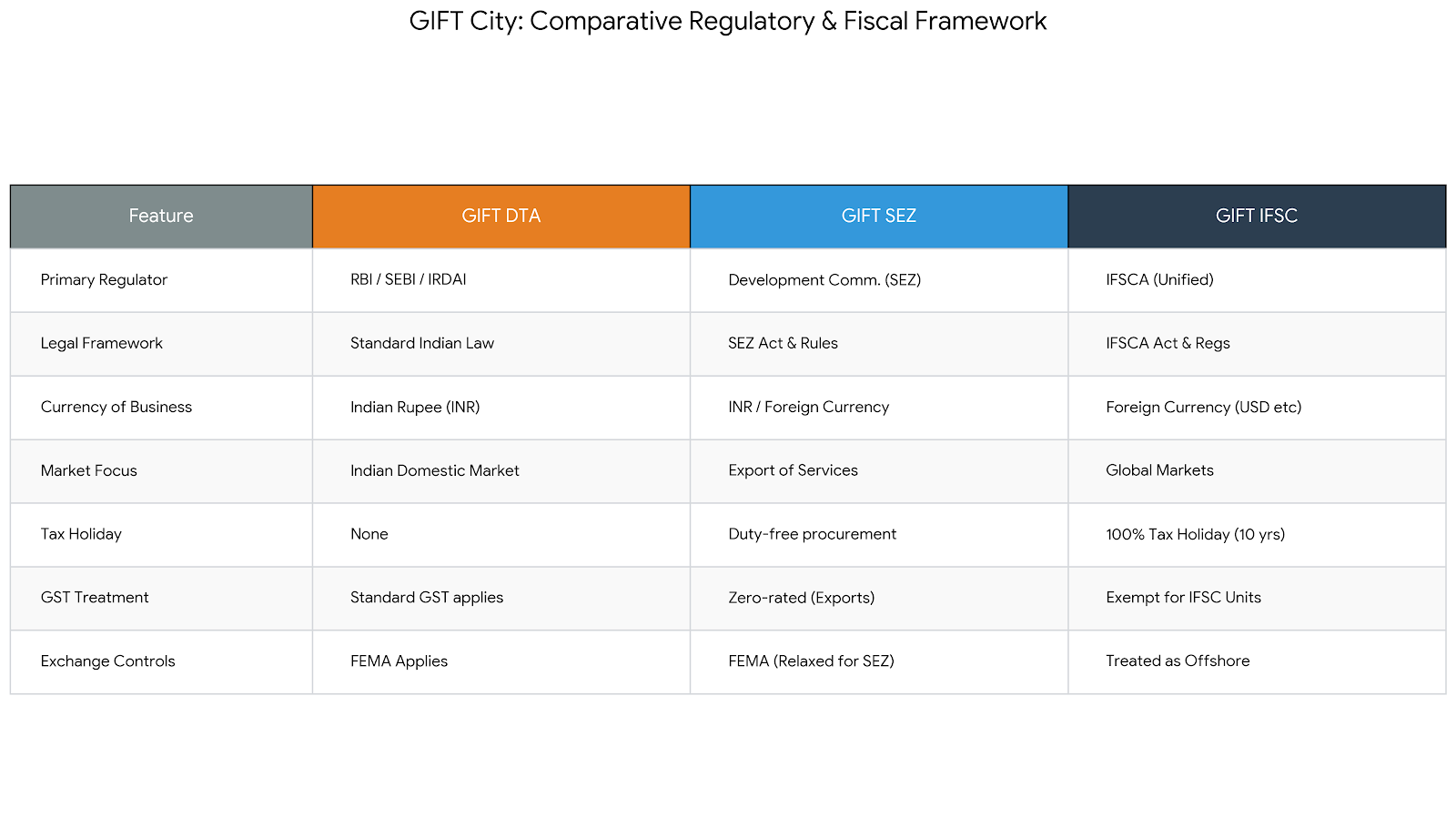

GIFT DTA is regulated exactly like any other Indian city. Companies operating in the DTA deal with the Ministry of Corporate Affairs for corporate law compliance, the Income Tax Department for direct taxation, GST authorities for indirect tax, and sector-specific Indian regulators where applicable. There is no involvement of SEZ authorities or the IFSC regulator at any stage. From a legal standpoint, GIFT DTA offers infrastructure and ecosystem advantages, but it does not alter the regulatory or tax character of the business in any way. A company in GIFT DTA is, for all practical purposes, in domestic India.

GIFT SEZ operates under a different logic altogether. It is governed by the SEZ Act and SEZ Rules, with supervision by the Development Commissioner and customs authorities. The regulatory focus here is not on the sector in which the business operates, but on whether the activity qualifies as an authorised operation and whether it results in export of services and foreign exchange earnings. A software development company, analytics firm, or global capability centre in GIFT SEZ is regulated as an SEZ unit, not as a financial services entity. Its compliance obligations arise from export performance, customs controls, and GST zero-rating requirements, not from any financial sector regulator. Being located in GIFT City does not, by itself, trigger RBI, SEBI, or IFSCA oversight for such businesses.

GIFT IFSC represents a complete departure from both the DTA and SEZ models. It is regulated by the International Financial Services Centres Authority, a unified financial regulator created specifically for IFSC operations. IFSCA performs functions analogous to those of RBI, SEBI, IRDAI, and PFRDA—but strictly in relation to activities carried out within the IFSC framework. Any entity seeking to operate in IFSC must first ensure that its proposed activity is recognised as a financial service under IFSCA regulations and must then obtain a licence or registration. Without such licensing, there is no legal basis to operate as an IFSC unit, irrespective of the office location or client base.

A point that is frequently misunderstood is the asymmetrical compliance overlap between IFSC and SEZ. An IFSC entity is required to comply not only with IFSCA regulations but also with certain SEZ-related operational requirements, such as authorised operations, bonded area conditions, and customs procedures. This is because IFSC is physically housed within the SEZ framework. However, the reverse is not true. A GIFT SEZ unit has no obligation to comply with IFSC regulations, obtain IFSCA licences, or meet financial sector compliance standards merely because it operates within GIFT City.

This one-directional compliance structure is central to understanding GIFT City. Misreading it leads businesses to overestimate regulatory flexibility in IFSC or underestimate the compliance intensity that comes with financial sector licensing. When regulatory jurisdiction is correctly identified at the outset, approvals, compliance planning, and tax positioning become predictable. When it is misunderstood, the result is often regulatory rejection or post-setup restructuring.

Business Eligibility: Who Can Actually Operate in Each Zone

GIFT IFSC: Financial Services Only — No Exceptions in Substance

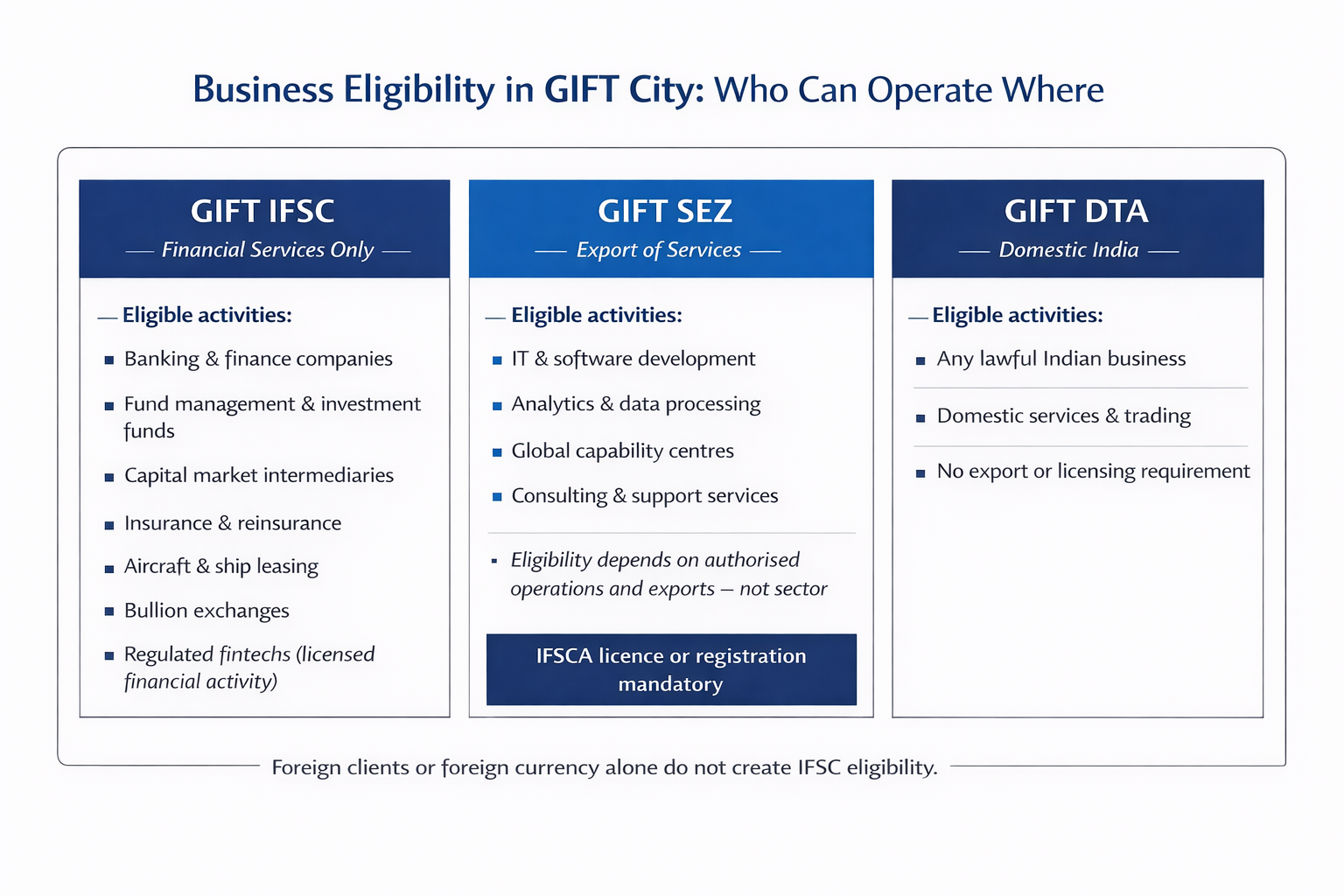

GIFT IFSC has been conceived as India’s offshore financial jurisdiction, and its design is deliberately narrow. It is not a general business zone, nor is it an international trade park in the conventional sense. The IFSC framework permits only those activities that qualify as international financial services under IFSCA regulations, and every operating entity must be licensed or registered accordingly. Banking units, finance companies, fund management entities, insurance and reinsurance businesses, capital market intermediaries, aircraft and ship leasing entities, bullion exchanges, and certain categories of regulated fintechs fall squarely within this framework because their activities are recognised as financial services and are capable of regulatory supervision.

What determines eligibility is not how global, sophisticated, or technology-driven the business appears, but whether the underlying activity is expressly recognised as a financial service by the IFSC regulator. This distinction is often misunderstood. A business does not become eligible for IFSC merely because it serves overseas clients, earns foreign currency, or operates in a cross-border context. If the activity does not require an IFSCA licence, it does not legally belong in IFSC, regardless of how compelling the commercial rationale may seem.

This is where many structuring assumptions fail in practice. Pure IT companies, backend software development teams, analytics and data processing firms, SaaS platforms, consulting businesses, law firms, accounting and tax advisory firms, HR service providers, marketing agencies, and trading entities are frequently proposed for IFSC on the assumption that foreign clientele or offshore billing is sufficient. It is not. These activities are not financial services in regulatory terms, and therefore cannot be undertaken as IFSC units, even if every client is located outside India.

The term “fintech” is another source of frequent confusion. Labeling a business as fintech does not automatically qualify it for IFSC. Unless the business model involves regulated financial intermediation—such as lending, asset management, capital market participation, insurance, payments infrastructure, or another activity specifically recognised under IFSCA norms—it will not withstand regulatory scrutiny. Technology may be an enabler of financial services, but technology by itself is not the service. In IFSC, the regulator licenses the financial activity, not the sophistication of the platform.

In effect, IFSC draws a clear and intentional boundary. It welcomes financial services in all their modern forms, but it excludes businesses whose core activity lies outside the regulated financial domain. Understanding this boundary at the outset is essential, because no amount of post-facto restructuring can convert a non-financial business into an IFSC-eligible one without fundamentally changing its activity.

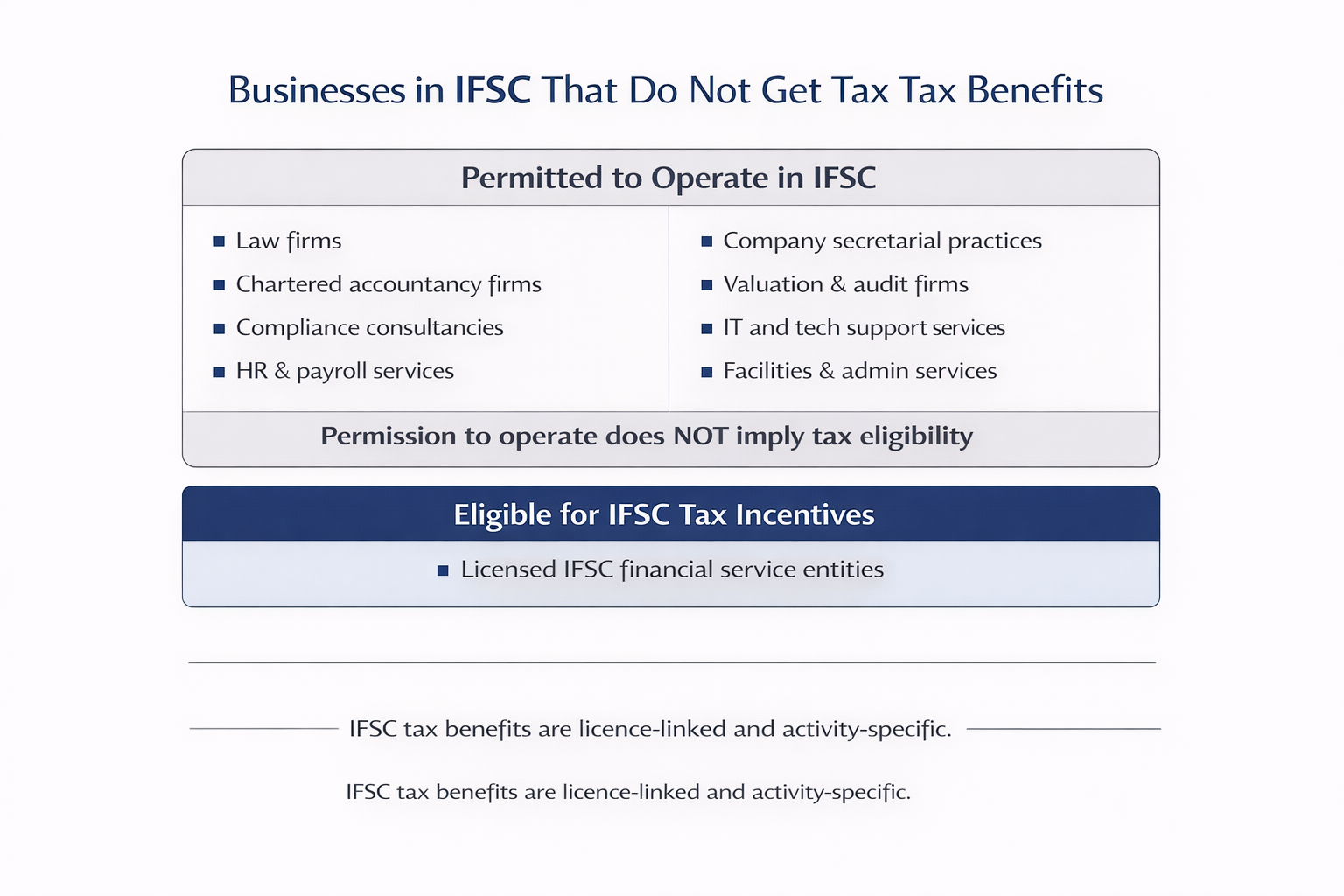

Businesses in IFSC That Do Not Get Tax Benefits

A common misconception in GIFT City structuring is that physical presence within the IFSC automatically carries tax privileges. In reality, IFSC tax incentives are activity-specific and licence-linked, not location-driven. Ancillary Service Providers (ASPs) are only the most visible example of this distinction. Several other categories of businesses may be permitted to operate within the IFSC ecosystem, yet remain entirely outside the IFSC tax incentive framework.

Professional firms—such as law firms, chartered accountancy firms, company secretarial practices, valuation firms, internal audit providers, and compliance consultancies—are typically allowed to operate in IFSC only to the extent they support licensed IFSC entities. Their presence is recognised as necessary for the functioning of the financial ecosystem, but they are not treated as financial service units in their own right. Consequently, their income does not qualify for the IFSC income-tax holiday, normal income-tax rates apply, and GST is chargeable in accordance with the general GST law. From a fiscal perspective, these firms remain fully domestic, notwithstanding their IFSC address.

The same principle applies to operational and support functions. Services such as human resources management, payroll processing, administrative outsourcing, facilities management, internal IT support, and office operations are often housed within IFSC premises for convenience or proximity to financial units. However, these activities are functionally supportive rather than regulatorily recognised financial services. As a result, they do not receive IFSC tax treatment. Their location inside IFSC serves an operational purpose, not a fiscal one.

This distinction becomes particularly important in group structures. Even within regulated financial groups, shared service centres, technology development teams, analytics units, or back-office operations are frequently excluded from IFSC incentives if their activities are not directly covered by an IFSCA licence. In practice, regulators and tax authorities look at the substance of the activity, not its proximity to a financial entity. Recognising this, many sophisticated groups deliberately separate functions: the fund, bank, or finance company operates as a licensed IFSC unit, while technology, analytics, and operational support are housed in a GIFT SEZ unit where export-linked benefits are more appropriate.

The underlying principle is consistent across all such cases. IFSC incentives are designed to promote international financial services, not to create a blanket low-tax zone for all businesses operating nearby. Permission to operate within the IFSC ecosystem should not be confused with entitlement to IFSC tax benefits. Understanding this distinction early allows businesses to design structures that are both compliant and commercially efficient, rather than discovering post-setup that expected incentives were never legally available.

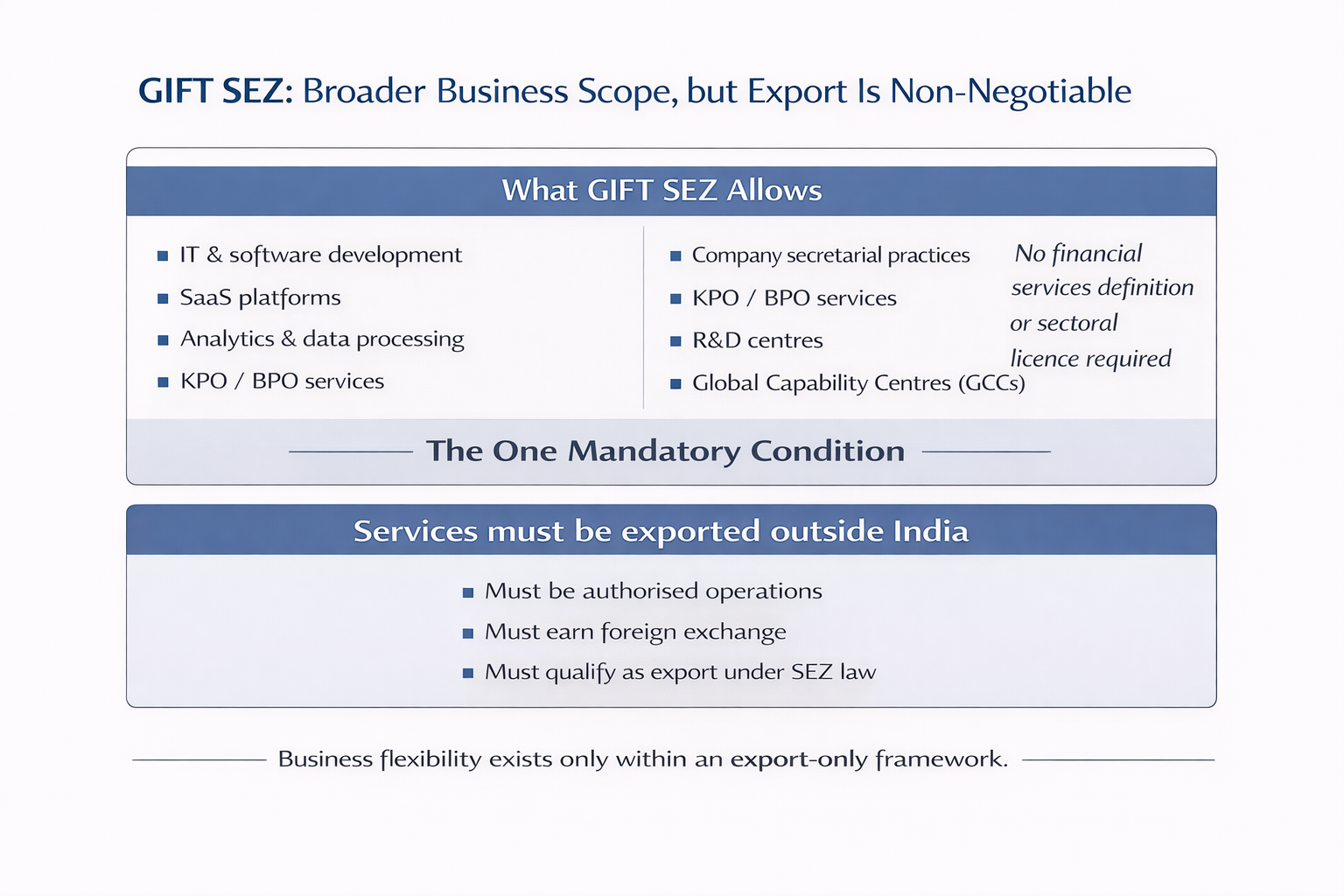

GIFT SEZ: Broader Business Scope, but Export Is Non-Negotiable

GIFT SEZ is designed as an export-oriented services enclave, not as a financial services jurisdiction. Its regulatory logic flows from the SEZ Act, which is built around the promotion of exports and foreign exchange earnings rather than sector-specific regulation. As a result, the scope of permissible business activity in GIFT SEZ is significantly broader than in IFSC, provided the services qualify as exports under SEZ law.

In practice, this makes GIFT SEZ a natural home for IT services, software development companies, SaaS platforms, analytics and data processing firms, KPOs and BPOs, research and development centres, and global capability centres. These businesses are not required to fit into any financial services definition, nor do they need a sectoral licence. What they must demonstrate, however, is that their output is exported outside India and that the activity forms part of their authorised operations approved under the SEZ framework.

A critical but often overlooked aspect of the GIFT SEZ framework is that services provided to IFSC units are treated as exports. Under SEZ and GST principles, IFSC entities are regarded as offshore for this purpose. This creates a commercially efficient structure for groups operating in GIFT City, where regulated financial entities are housed in IFSC while their technology, analytics, risk modelling, or back-office teams operate from a SEZ unit. The SEZ unit remains export-compliant, while the IFSC entity receives operational support without triggering domestic tax or GST leakage.

The export condition, however, is non-negotiable. The moment a GIFT SEZ unit begins billing Indian clients, servicing the domestic market, or operating a mixed business model where domestic and export activities are not clearly segregated, the SEZ framework begins to unravel. Domestic billing can jeopardise authorised operations, disrupt GST zero-rating, and expose the unit to clawback of benefits. SEZ law is unforgiving on this point because the incentive structure is premised entirely on exports.

For this reason, GIFT SEZ works best for businesses that are structurally export-oriented or that can cleanly ring-fence export activities. Where the business model is primarily India-facing, or where domestic and overseas services are inseparable, GIFT SEZ is usually the wrong jurisdiction, regardless of the infrastructure or tax appeal.

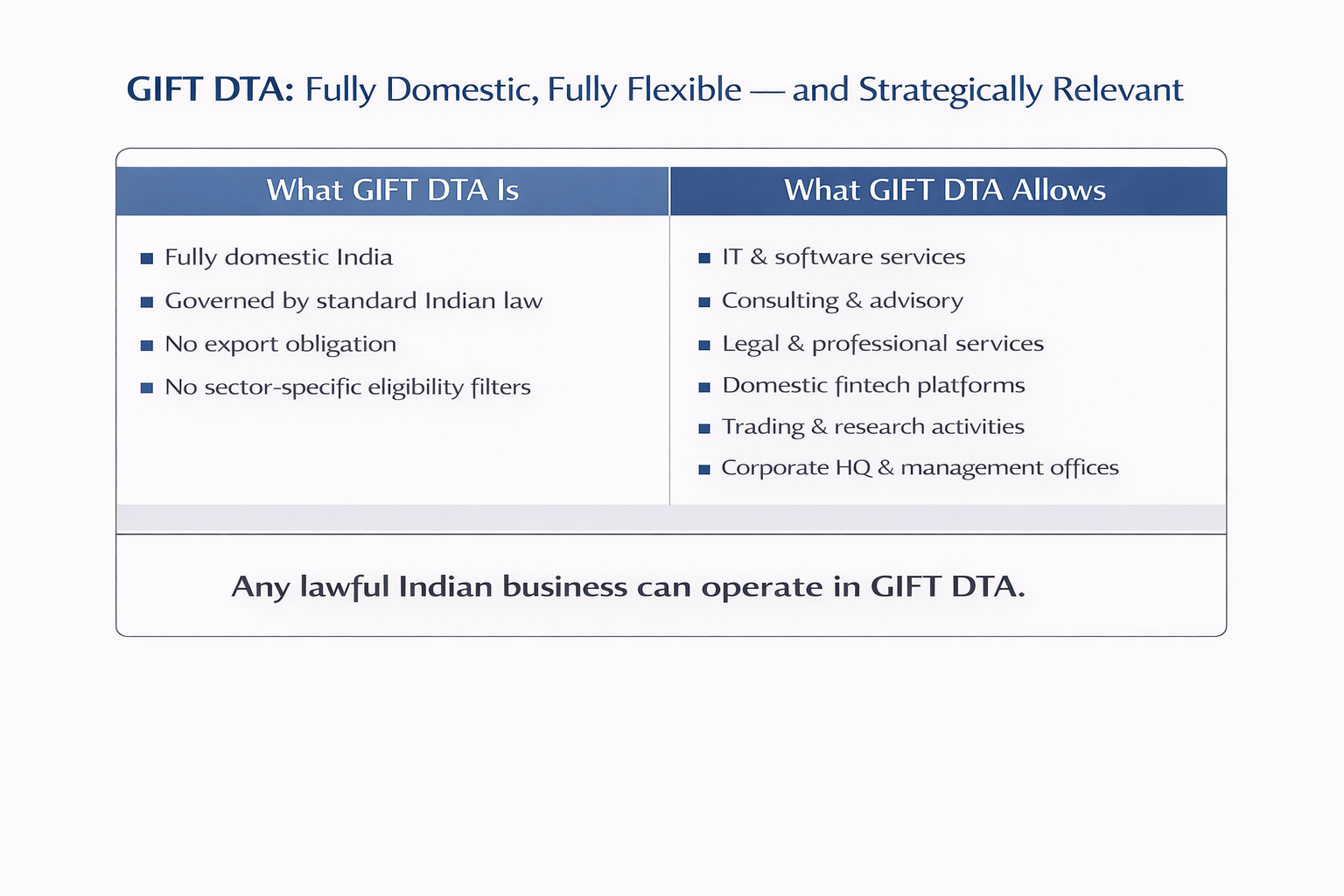

GIFT DTA: Fully Domestic, Fully Flexible — and Strategically Relevant

GIFT DTA represents the most flexible jurisdiction within GIFT City from a business eligibility perspective, and while it does not offer offshore tax treatment or central tax holidays, it would be a mistake to view it as merely a default or inferior option. For certain categories of businesses and group structures, GIFT DTA is not just suitable—it is strategically optimal.

From a legal standpoint, GIFT DTA is fully domestic India. Any lawful business activity can operate here, including IT services, consulting and advisory work, legal and professional services, domestic fintech platforms, trading activities, research functions, and corporate headquarters or management offices. There are no export obligations, no sector-specific licensing thresholds unique to the zone, and no requirement to align the business model to SEZ or IFSC policy objectives. This makes GIFT DTA the most operationally flexible part of GIFT City.

It is true that GIFT DTA does not provide offshore tax treatment. Income tax, GST, FEMA, and corporate laws apply in the same manner as they would in Mumbai, Bengaluru, or Delhi. However, this is precisely what makes GIFT DTA attractive for businesses whose operations are inherently India-facing or whose models do not cleanly fit into export or financial services frameworks. For such businesses, regulatory certainty often matters more than notional tax incentives.

One of the most tangible advantages of GIFT DTA is proximity without regulatory entanglement. Businesses can locate themselves within the GIFT City ecosystem—physically close to IFSC funds, banks, insurers, and SEZ units—without subjecting themselves to IFSC licensing or SEZ compliance. This is particularly valuable for professional firms, advisory practices, domestic fintechs, consulting businesses, and group management teams that need regular interaction with IFSC entities but cannot, and should not, operate under IFSC regulations.

GIFT DTA also benefits from state-level and zone-specific facilitation measures, even though it does not enjoy central tax holidays. These include faster approvals, simplified local permissions, superior digital infrastructure, reliable utilities, and a business environment designed around financial and professional services. While these incentives are not codified as income-tax exemptions, they materially reduce operational friction and time-to-market—an advantage that is often underestimated in tax-only comparisons.

For group structures, GIFT DTA frequently plays a deliberate and important role. It is commonly used to house Indian management teams, domestic advisory functions, compliance and governance offices, or client-facing operations, while regulated financial activities sit in IFSC and export-oriented technology or analytics teams operate from SEZ units. In such structures, GIFT DTA provides stability and flexibility, allowing other entities in the group to preserve their specialised regulatory status without contamination.

The key point is this: GIFT DTA is not chosen for tax arbitrage, but for structural coherence. Where a business does not qualify for IFSC incentives or cannot meet SEZ export conditions, forcing it into those frameworks creates regulatory risk without commensurate benefit. In those cases, GIFT DTA is not the compromise option—it is the correct one.

Including this perspective in any serious discussion of GIFT City is essential. Without it, DTA appears unattractive by comparison, when in reality it often serves as the backbone of well-designed, compliant, and scalable GIFT City structures.

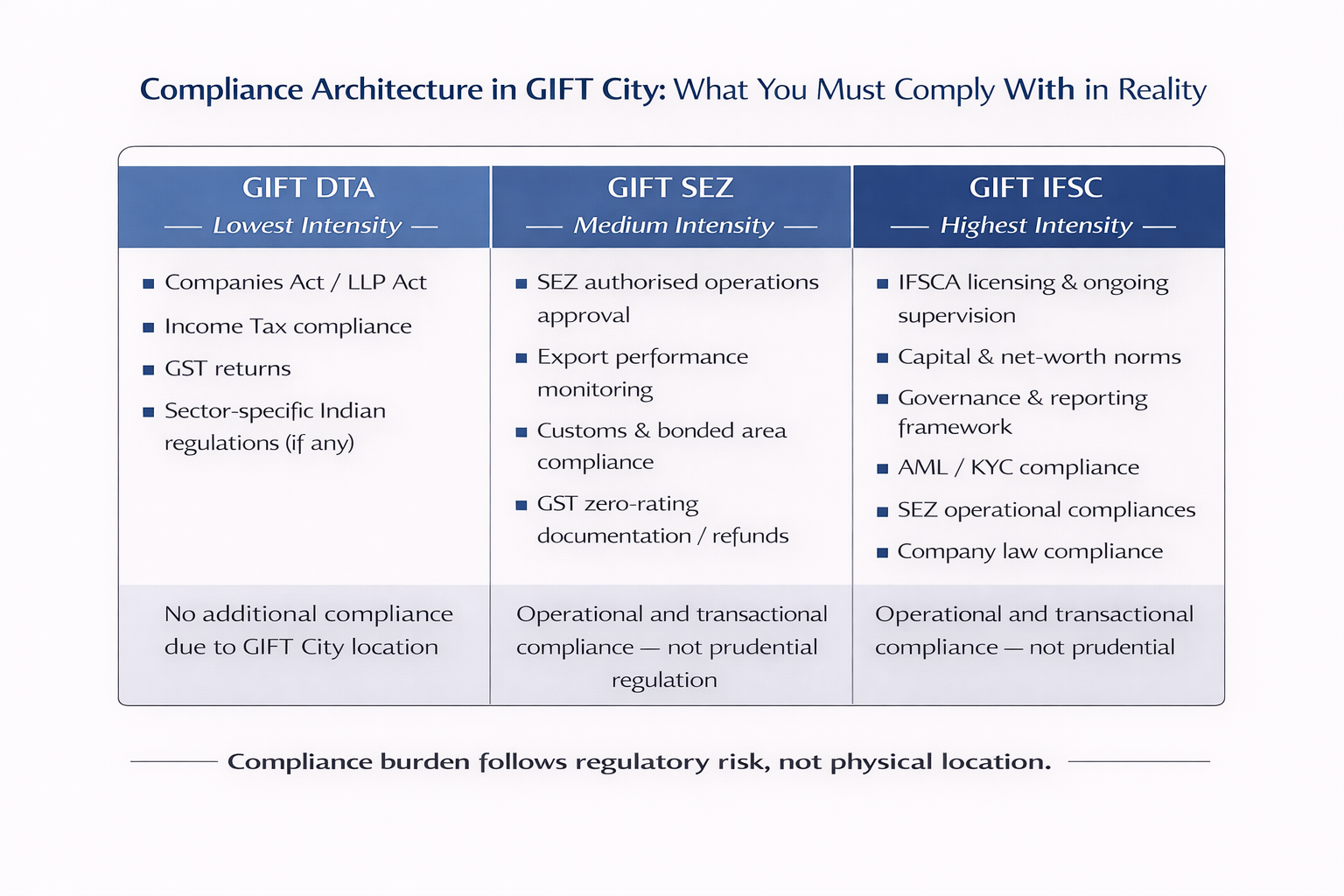

Compliance Architecture: What You Must Comply With in Reality

Compliance obligations within GIFT City vary sharply depending on the jurisdiction in which an entity operates. This is not accidental. Each zone is built around a different policy objective, and the compliance architecture reflects the level of regulatory risk the law associates with that activity. As a result, entities in IFSC, SEZ, and DTA operate under materially different compliance intensities, even though they may be located in the same physical complex.

An IFSC entity carries the highest compliance burden within GIFT City, and this is by design. IFSC units operate in regulated financial markets, deal with cross-border capital, and interact with international investors and counterparties. Consequently, they must comply with IFSCA licensing conditions, minimum capital and net-worth norms, detailed governance frameworks, periodic regulatory reporting, and robust AML and KYC obligations. Regulatory supervision in IFSC is active and ongoing, not event-based. Most IFSC entities are required to appoint designated officers such as a Principal Officer, Compliance Officer, Risk Officer, and AML Officer. These appointments are not merely formal; individuals are assessed on fitness and propriety standards, and the regulator expects real accountability attached to these roles.

In addition to IFSC-specific regulation, IFSC units are also subject to certain SEZ operational compliances, because the IFSC is physically situated within a Special Economic Zone. This includes obtaining approval for authorised operations, complying with bonded area and customs controls where applicable, and submitting periodic performance reports to SEZ authorities. On top of this, standard company law or LLP compliance continues to apply—board governance, statutory audits, filings, and disclosures are not relaxed merely because an entity operates in IFSC. The result is a layered compliance framework that is sophisticated, predictable, and globally aligned, but undeniably demanding.

SEZ entities operate under a significantly lighter compliance framework by comparison. Their obligations are primarily transactional and operational rather than prudential. Compliance revolves around adherence to authorised operations approved under the SEZ framework, maintenance of export performance, customs and duty-free import controls, and proper documentation for GST zero-rating or refunds. There is no sectoral regulator supervising the business model, no licensing of activities based on financial risk, and no requirement to appoint regulatory officers akin to those in IFSC. As long as export conditions are met and SEZ rules are followed, regulatory interaction remains limited and predictable.

DTA entities, finally, operate under standard Indian compliance norms with no additional overlay arising from their location in GIFT City. Corporate law compliance, income-tax filings, GST returns, and sector-specific Indian regulations apply exactly as they would elsewhere in the country. There are no special reporting obligations, no additional regulators, and no dual-layer oversight. This simplicity is one of the reasons DTA remains attractive for businesses that prioritise operational freedom and regulatory certainty over specialised incentives.

Understanding these differences at the outset is critical. Compliance intensity should be matched to the nature of the business and its risk profile. When businesses underestimate IFSC compliance or overestimate SEZ and DTA obligations, structures become misaligned. When compliance architecture is factored into the structuring decision from day one, GIFT City works as intended—each zone serving its distinct economic role without regulatory friction.

Tax and GST Benefits: Who Actually Gets What

The incentive framework within GIFT City is often misunderstood because it is discussed in broad strokes rather than through the lens of statutory entitlement. In reality, tax and GST benefits in GIFT City are not location-based incentives; they are jurisdiction- and activity-specific concessions granted to advance clearly defined policy goals. Understanding who actually qualifies for these benefits requires examining both the legal status of the entity and the nature of the activity it undertakes.

GIFT IFSC offers the most generous tax incentives, but these benefits are strictly limited to licensed financial service units operating under the IFSC regulatory framework. Eligible entities are entitled to a 100% income-tax exemption for ten consecutive years out of a block of fifteen years, allowing flexibility in tax planning during the growth phase. These units are also exempt from MAT and AMT, which is a significant departure from the normal Indian tax regime. In many cases, IFSC entities benefit from favourable withholding tax treatment on specified payments, and from a GST perspective, services provided to non-residents or other IFSC units are generally outside the GST net, resulting in near-complete GST neutrality for offshore financial services.

Crucially, these incentives attach to the licensed financial activity, not to the physical location within IFSC. Professional firms, support entities, ancillary service providers, and any business activity that is not directly licensed by IFSCA do not qualify for IFSC tax benefits, even if they operate from IFSC premises or exclusively service IFSC entities. Their income remains fully taxable under normal provisions, GST applies as per general law, and no income-tax holiday is available. This distinction is deliberate: IFSC incentives are intended to promote international financial intermediation, not to create a broad-based low-tax enclave for all businesses operating nearby.

GIFT SEZ follows a different incentive logic. Tax benefits here are export-linked rather than sector-linked. Income derived from eligible exports of services enjoys phased income-tax deductions under the SEZ framework, subject to satisfaction of prescribed conditions. From a GST standpoint, exports from SEZ units are zero-rated, allowing units to operate without GST cost leakage, either through exemption mechanisms or refunds. Additionally, imports of goods and services for authorised operations are permitted without payment of customs duties or GST. These benefits can be substantial, but they are conditional on strict adherence to export obligations and authorised operations under SEZ law. Any dilution of export character or commingling with domestic activity can erode or eliminate these incentives.

GIFT DTA, by contrast, does not offer central tax incentives. Entities operating in the DTA are subject to the standard Indian income-tax and GST regime, and there is no concept of offshore treatment or tax holiday. Any incentives available are typically limited to state-level concessions, such as reductions or exemptions in stamp duty, registration charges, or certain local levies. While these may lower entry or transaction costs, they do not alter the fundamental tax character of the business.

The broader takeaway is that tax and GST benefits in GIFT City are purpose-built tools, not universal entitlements. They reward specific types of economic activity—international financial services in IFSC and exports in SEZ—while deliberately excluding activities that fall outside those objectives. Businesses that align their structures with these policy goals benefit meaningfully. Those that assume incentives will apply simply because of location often discover, post-setup, that the law never supported that expectation.

The Structuring Reality Most Brochures Won’t Tell You

In real-world implementations, well-structured business groups rarely attempt to collapse all activities into a single GIFT City entity, particularly not into IFSC. Despite the marketing narrative, IFSC is not designed to be an all-purpose offshore hub. It is a specialised regulatory environment for licensed financial activity, and regulators are acutely sensitive to attempts to stretch that boundary. Groups that try to house technology teams, advisory functions, or support services within IFSC purely to access tax benefits almost invariably encounter regulatory resistance—either at the licensing stage or during subsequent supervisory reviews.

Experienced practitioners therefore approach GIFT City as a modular ecosystem, not as a one-entity solution. Regulated financial activity—such as fund management, lending, insurance, or leasing—is placed squarely within IFSC, where it can operate under a clear licensing framework and legitimately access IFSC incentives. Technology development, analytics, risk modelling, and back-office functions are commonly housed in GIFT SEZ, where the export-oriented framework is better suited to such activities and tax and GST benefits flow naturally from the export character of the services. Domestic advisory, management, governance, and India-facing functions are often located in GIFT DTA, where regulatory flexibility and certainty outweigh the absence of tax holidays.

Attempts to extract IFSC tax benefits for non-financial or support activities usually fail because regulators and tax authorities look at substance over form. If an activity does not require an IFSCA licence and does not expose the entity to financial sector risk, it is unlikely to be treated as an IFSC-eligible business, regardless of how closely it supports a financial unit. This is not a grey area in practice; it is an enforcement reality.

The real advantage of GIFT City, therefore, lies not in blanket incentives or aggressive consolidation, but in precision zoning—placing each business activity in the jurisdiction it legally belongs to and allowing each zone to perform the function it was designed for. When structures respect these boundaries, approvals become smoother, compliance becomes predictable, and tax benefits are defensible. When they do not, GIFT City quickly loses its appeal, not because the framework is flawed, but because it has been misunderstood.

GIFT City’s strength does not lie in offering universal tax concessions or a one-size-fits-all offshore solution. Its real power comes from the fact that it provides three distinct regulatory instruments within a single ecosystem, each designed to serve a specific economic purpose. When businesses approach GIFT City with regulatory discipline—identifying the correct jurisdiction, aligning their activity with the applicable legal framework, and structuring with realistic expectations—the framework works exceptionally well.

Conversely, when GIFT City is treated as a tax shortcut or a branding exercise, the results are predictably disappointing. Licences are delayed or denied, expected incentives fail to materialise, and structures require post-facto correction. In that sense, GIFT City rewards precision and penalises assumption. Businesses that understand this from the outset are far more likely to build compliant, scalable, and regulatorily resilient operations within the GIFT ecosystem.

About the Author

Prashant Kumar is a Company Secretary and Partner at Eclectic Legal, advising Indian and global clients on GIFT IFSC licensing, SEZ structuring, FEMA-compliant cross-border models, and regulatory governance frameworks. He works closely with funds, fintech companies, IT and software businesses, professional firms, and multinational groups to design compliant and commercially sound structures within GIFT City.

📞 +91-9821008011 ✉️ prashant@eclecticlegal.com

Frequently Asked Questions (FAQs)

1. Can a non-financial business ever legitimately operate from GIFT IFSC?

In substance, no. GIFT IFSC is a licensed financial jurisdiction, not a general international business zone. An entity can operate from IFSC only if its core activity qualifies as a financial service recognised under regulations issued by the International Financial Services Centres Authority and the entity holds the requisite licence or registration. Merely serving foreign clients, earning foreign currency, or supporting a financial institution does not make an activity eligible.

There are limited cases where non-financial entities such as professional firms or support providers are permitted physical presence in IFSC, but this permission is functional, not fiscal. These entities are not treated as IFSC units for tax or regulatory purposes and do not enjoy IFSC incentives. The legal test is always the same: is the activity itself a regulated financial service? If the answer is no, IFSC is not the correct jurisdiction.

2. Do all IFSC-licensed entities automatically get tax holidays and GST exemptions?

No. Even within IFSC, tax benefits are not automatic and do not apply uniformly across all entities or all income streams. The income-tax holiday, MAT/AMT exemption, and GST neutrality apply only to income derived from approved, licensed financial services activities carried out in accordance with IFSC regulations. Any income that falls outside the licensed scope may be taxed under normal provisions.

Further, IFSC incentives do not extend to professional firms, ancillary service providers, shared service centres, or support entities, even if they operate exclusively for IFSC clients. The tax law follows the nature of the activity, not the address. This distinction becomes especially important during assessments and audits, where authorities examine substance over form.

3. Is GIFT SEZ suitable for businesses with both Indian and foreign clients?

Generally, no—unless the business can clearly segregate its export and domestic activities. GIFT SEZ is fundamentally an export-oriented framework, and its tax and GST benefits are contingent on services being exported outside India. The moment a unit begins servicing Indian clients or billing domestically without clear ring-fencing, it risks breaching SEZ conditions.

In practice, SEZ works best for businesses that are structurally export-focused or can maintain a clean separation between export operations and domestic business. Where such separation is not feasible, operating from GIFT DTA is usually safer and more compliant, even if it means foregoing SEZ tax benefits.

4. Why do many groups use all three zones—IFSC, SEZ, and DTA—together?

Because each zone is designed to perform a different economic and regulatory function, and combining them often produces the most efficient structure. IFSC is used for regulated financial activity such as fund management, lending, insurance, or leasing. SEZ is used for export-oriented technology, analytics, risk modelling, or back-office services. DTA is used for domestic advisory, management, governance, or India-facing operations.

This layered approach aligns each activity with the jurisdiction it legally belongs to, avoids regulatory friction, and ensures that incentives—where available—are defensible. Groups that try to compress all activities into IFSC usually face regulatory pushback; those that respect zoning logic tend to scale smoothly.

5. Does operating from GIFT DTA provide any advantage if there are no major tax incentives?

Yes, but the advantages are structural rather than fiscal. GIFT DTA offers regulatory certainty, operational flexibility, and proximity to IFSC and SEZ entities without imposing additional compliance burdens. For professional firms, domestic fintechs, advisory businesses, and group management teams, this combination is often more valuable than a tax holiday that does not legally apply.

Additionally, GIFT DTA benefits from state-level facilitation, superior infrastructure, and an ecosystem built around financial and professional services. For many businesses, especially those that are India-facing by nature, GIFT DTA is not a compromise—it is the correct jurisdiction.

6. What is the most common mistake businesses make when choosing a GIFT City zone?

The most common mistake is starting with tax benefits instead of regulatory eligibility. Businesses often ask where the incentives are highest and then try to force their model into that zone. In GIFT City, this approach almost always backfires. Licences are denied, benefits are disallowed, or structures need to be unwound later.

The correct approach is to first identify the legal character of the activity—financial service, export service, or domestic business—and then choose the zone that was designed for that activity. When this sequence is followed, benefits flow naturally. When it is reversed, GIFT City becomes unnecessarily complex.

[…] City Explained Properly: Understanding GIFT DTA, GIFT SEZ and GIFT IFSChttps://csatwork.in/gift-city-dta-sez-ifsc-explained/A regulatory and compliance-focused explanation of how GIFT City is really organised. This article […]