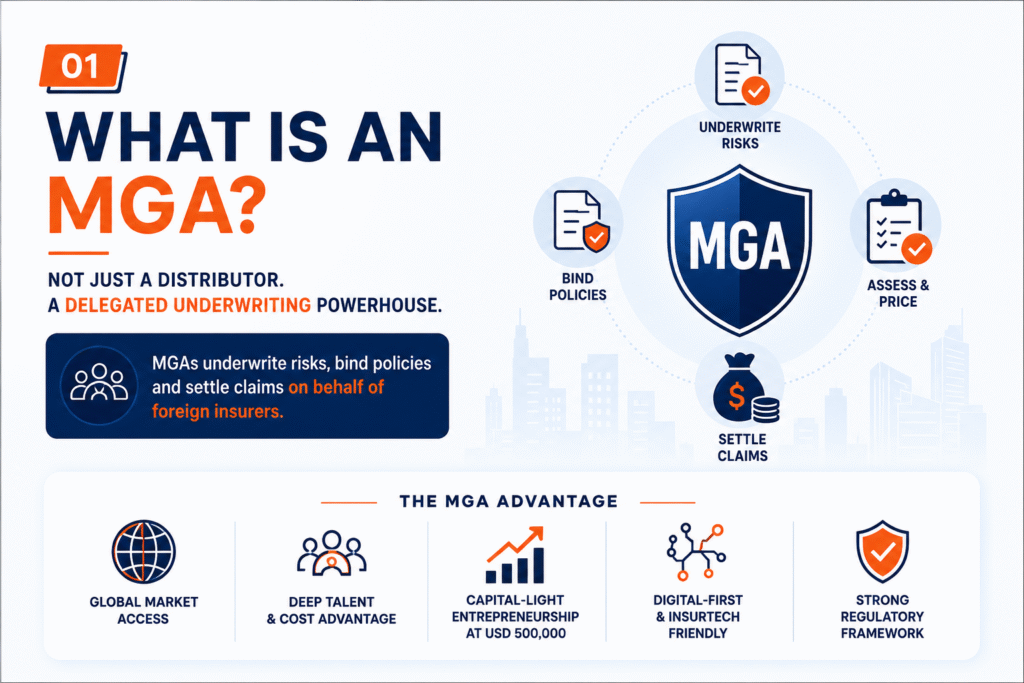

On 8 June 2026, the International Financial Services Centres Authority (IFSCA) notified the IFSCA (Managing General Agents) Regulations, 2026, creating — for the first time in India — a dedicated, stand-alone regime for Managing General Agents (MGAs) at GIFT IFSC. An MGA is an insurance intermediary that holds delegated authority from a foreign insurer to underwrite direct insurance risks and/or settle claims on the insurer’s behalf. Entry capital is USD 500,000, the framework is built around a Binding Authority Agreement (BAA), and MGAs may write business in the IFSC and offshore — but not in India’s Domestic Tariff Area. This positions GIFT City as a credible global coverholder/MGA hub, competing with Lloyd’s, DIFC and Singapore.

What exactly is a Managing General Agent (MGA)?

This is the conceptual heart of the regulation, and it is genuinely new for India.

A traditional Indian intermediary — broker or agent — distributes. It cannot price a risk, bind cover, or pay a claim. An MGA can. Under these Regulations, an MGA is an insurance intermediary that exercises delegated authority from a foreign insurer to:

- underwrite direct insurance risks (assess, accept/reject, bind, issue binders, price), and/or

- settle claims within agreed monetary limits.

This is the global “coverholder” model that powers the Lloyd’s and London specialty market and a fast-growing share of US and European specialty premium. India did not previously have a recognised home for it. The MGA effectively functions as the insurer’s outsourced underwriting and claims engine — without itself carrying the insurance risk, which stays with the foreign insurer.

The legal hooks are worth noting for advisory work: the Regulations draw power from Section 28(1) read with Sections 12 & 13 of the IFSCA Act, 2019, and Sections 42D, 42E and 118A of the Insurance Act, 1938. They also carve MGAs out of the earlier patchwork — the MGA provisions in the IFSCA (Registration of Insurance Business) Regulations, 2021 stand omitted, and the Insurance Intermediary Regulations, 2021 will no longer apply to MGAs.

Who can set up an MGA in GIFT IFSC? (Eligibility)

There are two entry routes:

Route 1 — Branch of an existing foreign MGA. A body corporate already registered/licensed for MGA-type activity abroad can set up a branch in the IFSC, provided it holds a valid home licence, has a track record of acting as an agent (solicitation, underwriting, claims), is based in a DTAA jurisdiction, and obtains a No-Objection Certificate from its home regulator.

Route 2 — New company in the IFSC. Anyone else must incorporate a company under the Companies Act, 2013inside the IFSC. Note: LLPs are expressly excluded — the definition of “body corporate” carves out limited liability companies.

A critical gating condition: at the application stage, the applicant must already have at least one written contract with a foreign insurer to manage part of its direct insurance business.

The foreign insurer itself must clear a high bar:

| Foreign insurer eligibility | Requirement |

|---|---|

| Registration | Licensed for direct insurance in home country |

| Net worth | Minimum USD 100 million |

| Credit rating | ‘A’ or equivalent for the last 3 years |

| Jurisdiction | DTAA country; not FATF “high-risk, call for action” |

| Track record | Satisfactory regulatory/supervisory record |

| Commitment | Board resolution undertaking to meet IFSC liabilities |

Capital, net worth, deposit and fees — the cost of entry

This is deliberately capital-light relative to a full insurer/branch, which is the commercial point.

| Parameter | Requirement |

|---|---|

| Paid-up equity (company) / assigned capital (branch) | USD 500,000 with an IFSC Banking Unit (IBU) |

| Net worth | Higher of USD 250,000 or 50% of capital (branch maintains at parent level) |

| Security deposit | USD 10,000 + 10% of capital, lien to IFSCA (separate cap up to USD 100,000) |

| Application fee | USD 1,000 (non-refundable) |

| Registration fee | USD 5,000 (non-refundable) |

| Annual fee | Higher of USD 12,500 or 0.05% of GWP |

| Time to commence | 180 days (extendable to a maximum of 18 months) |

Two structuring points advisors should flag: promoter investment must come from owned funds, not borrowings, and shares cannot be pledged for credit. Professional Indemnity cover — including cyber liability, retroactive/continuous cover and ombudsman/arbitration awards — is mandatory throughout registration, with tiered excess caps depending on whether the MGA holds client money.

How the model actually works: the Binding Authority Agreement (BAA)

No MGA can solicit, underwrite or settle a single claim until a BAA — containing the mandatory Schedule-IV clauses — is executed with the foreign insurer and filed with IFSCA. The BAA is the operating licence in commercial terms. It must spell out classes of business, territorial limits, per-risk liability caps, underwriting guidelines, rating basis, and the underwriting capacity allocated.

Key guardrails that define the risk perimeter:

- The BAA must distinguish “Claims Processing” from “Claims Settlement” as separate delegated functions.

- Any claim above USD 10,000 or involving a coverage dispute must go back to the foreign insurer for prior approval.

- A foreign insurer cannot delegate more than 10% of its previous-year GWP to a single MGA — a concentration cap.

- The MGA must notify the insurer if quarterly GWP crosses 5% of the insurer’s policyholder surplus.

Fiduciary accounts: bankruptcy-remote client money

Where the MGA collects premium or claim funds, the money sits in a Fiduciary Account with an IBU, segregated per foreign insurer. Crucially, this money is not attachable and does not form part of the MGA’s assets on insolvency or liquidation — strong policyholder and insurer protection. The MGA cannot hold more than three months of losses and loss-adjustment expenses; surplus is remitted monthly. A statutory-auditor certificate confirming segregation is filed half-yearly.

What MGAs can and cannot do

Permitted (Schedule I): underwriting and risk selection; product design and drafting of wordings; full policy lifecycle administration; fiduciary and accounting functions; and delegated claims management. Digital distribution — self-network platforms, linking to insurers’ web portals, and tele-marketing — is expressly allowed.

Prohibited (Reg 11):

- Binding reinsurance or retrocession for the insurer

- Participating in insurance/reinsurance syndicates

- Sub-delegating underwriting/claims authority (no chaining)

- Jointly employing someone already employed by the foreign insurer

- Soliciting from the Domestic Tariff Area (rest of India), except per Section 2CB of the Insurance Act

- Multi-level marketing

Operations run in Specified Foreign Currency; an INR account is allowed only for administrative and statutory expenses.

Governance and compliance you can’t skip

- Principal Officer / Branch Head must be in direct employment, resident in India, and “fit and proper”.

- Board-approved underwriting & claims policy (reviewed every 3 years) and conflict-of-interest policy (reviewed annually).

- Data localisation: policyholder data must be stored within India (including IFSCs).

- Foreign insurer must run an annual independent audit and half-yearly on-site review of the MGA’s underwriting and claims, plus an annual actuarial opinion on loss reserves.

- Robust cyber security and resilience framework; full related-party disclosure in audited accounts.

The real opportunity: why this matters commercially

This is where the regulation moves from compliance text to strategy.

1. GIFT City becomes a delegated-authority domicile. India now has a recognised home for the global MGA/coverholder boom — a segment growing rapidly in the US, UK and Europe. The pitch competes directly with Lloyd’s, DIFC and Singapore, but with a deep, low-cost talent base.

2. Capital-light entrepreneurship for underwriters. At USD 500,000, a specialist underwriting team can launch a regulated MGA without the balance sheet of an insurer. Expect entrepreneurial “lift-outs” — experienced underwriters building niche books backed by foreign capacity.

3. Specialty and emerging lines. MGAs globally win in cyber, parametric, marine, trade credit, political risk, D&O, SME and embedded insurance. India can build genuine product and pricing IP here, not just back-office support.

4. Talent and cost arbitrage, formalised. India already runs global insurance operations via GCCs. The MGA licence lets that talent own the underwriting and claims decision — moving up the value chain from processing to authority.

5. Completing the GIFT insurance stack. GIFT already hosts reinsurers and foreign reinsurance branches. The MGA layer adds front-end distribution and underwriting capacity, making the ecosystem far more complete and self-reinforcing.

6. Tech-led and digital-first models. Self-network platforms, portal integration and tele-marketing are permitted — ideal for insurtech-style, data-driven MGAs serving international risks.

Watch-outs to price into any business plan: the book must be IFSC/offshore only (no domestic market), the 10% single-insurer concentration cap limits over-reliance on one capacity provider, sub-delegation is barred, and branch MGAs must hold net worth at parent level. The IFSC tax incentives under Section 80LA make the economics attractive — but that warrants a separate, fact-specific tax structuring view (and I’m not offering tax advice here, only flagging it).

Frequently asked questions

Is an MGA the same as an insurance broker?

No. A broker distributes and advises. An MGA holds delegated authority from the insurer to bind risks and settle claims — far closer to acting as the insurer’s outsourced underwriting and claims office.

Can an MGA in GIFT City sell insurance to customers in mainland India?

No. MGAs cannot solicit direct insurance business from the Domestic Tariff Area, except as permitted under Section 2CB of the Insurance Act, 1938. The business is IFSC and offshore.

What is the minimum capital to set up an MGA in GIFT IFSC?

USD 500,000 (paid-up equity for a company, or assigned capital for a branch), maintained with an IFSC Banking Unit.

Can an LLP register as an MGA?

No. LLPs are excluded; the entity must be a company or a branch of a foreign body corporate.

How long does an MGA have to start operations?

180 days from registration, extendable up to a maximum of 18 months.

This article is for general information and does not constitute legal advice. Specific structuring, tax and licensing decisions should be taken on a fact-specific basis.

About the Author

Prashant Kumar is a Company Secretary, published author, and corporate & financial-services regulation specialist with direct, on-ground experience in the GIFT IFSC ecosystem. He serves as Company Secretary and Compliance Officer at Global Horizons Capital Advisors (IFSC) Private Limited, an IFSCA-licensed Investment Banker at GIFT City — giving him a working line of sight into how IFSCA frameworks are actually structured, licensed and implemented on the ground.

His work spans IFSC entity setup, licensing and regulatory structuring, fund management (FME registration and AIF schemes), IPOs, listings, GIFT IFSC leasing structures, and end-to-end compliance for financial-services entities — the same regulatory machinery that now underpins new regimes like the IFSCA (Managing General Agents) Regulations, 2026.

For professional discussions on GIFT IFSC entity setup, licensing, and regulatory strategy — including MGA registration, IFSC structuring, and broader compliance gap-checks — Prashant and the team at Global Horizons Capital Advisors are positioned to provide structured, regulation-grounded advisory.

📞 +91 98210 08011 | ✉️ prashant.kumar@global-horizons.in

🔗 LinkedIn: csprashantkumar · WhatsApp Channel: Join here · Instagram: @pkforchange

Great content! Keep up the good work!

[…] (For the full regulatory breakdown of what an MGA can and cannot do, see our companion piece: IFSCA MGA Regulations 2026 Explained. […]